Why would you trade a pandemic-era mortgage rate for a higher one just to add a master suite or a garage? Many North Texas families mistakenly believe they must refinance their entire home to expand, but there are smarter home addition financing options Texas residents can use to keep their current low rates intact. It’s understandable to feel hesitant when national equity loan averages sit near 8.05% and the Texas Constitution limits your total debt to 80% of your home’s value.

You deserve a straightforward plan to fund your expansion without the fear of under-budgeting for structural surprises or getting lost in complex state regulations. We’ve built this guide to help you identify the specific loan types that fit your project goals, whether you are looking to build a detached ADU or a complex structural renovation. You’ll learn the essential differences between equity-based loans and specialized construction financing, the impact of the mandatory 12-day cooling-off period, and how to find a contractor who understands the intricate draw process required for large-scale projects.

Key Takeaways

- Understand why 2026 market conditions in North Texas make structural expansion a more stable investment than relocating and sacrificing your current mortgage rate.

- Compare the most effective home addition financing options Texas offers, specifically matching fixed-rate equity loans or flexible HELOCs to your project’s scope.

- Discover how to leverage construction loans to borrow against the “as-completed” value of your home, ensuring your budget reflects the future worth of your new master suite or ADU.

- Learn to protect your investment by using professional structural assessments and Tarrant Appraisal District data to prevent hidden costs and maximize ROI.

- Identify how the design-build model streamlines the financing draw process and see if you qualify for specialized incentives for teachers, first responders, and military families.

Understanding the Texas Home Addition Financing Landscape in 2026

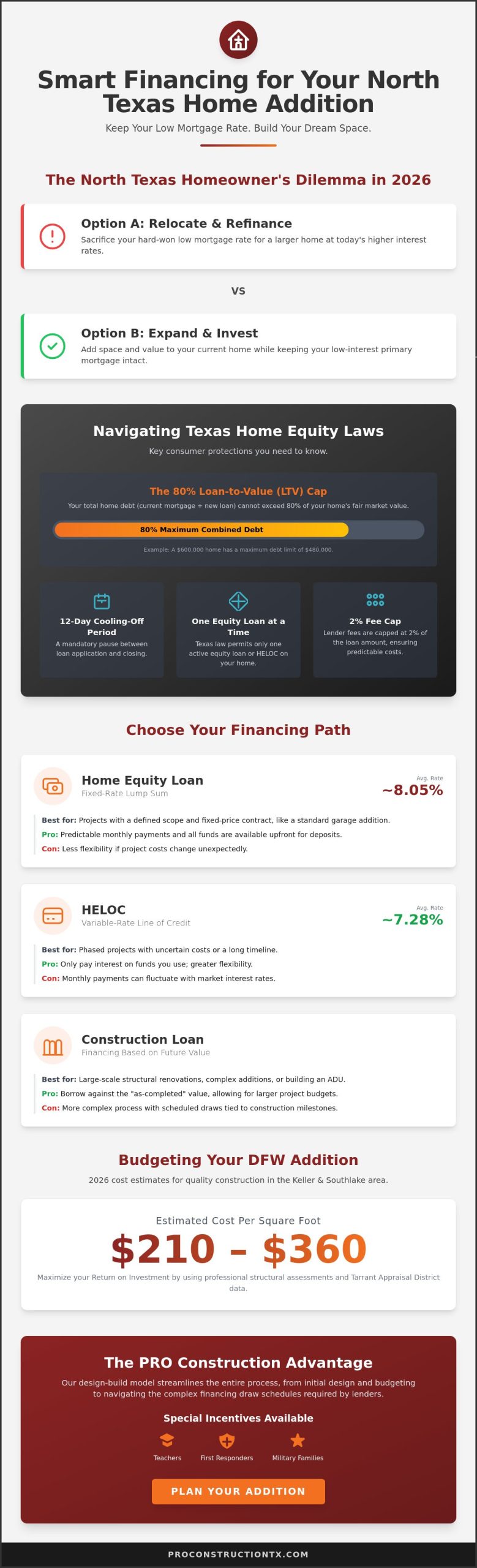

North Texas homeowners in 2026 are facing a unique crossroads. Most residents in Keller and Southlake are holding onto mortgage rates significantly lower than current market offerings. This makes traditional refinancing a poor financial move. Instead, families are looking for home addition financing options Texas lenders provide to expand their current footprint without losing their low-interest primary mortgages. Funding these projects generally falls into three categories. First are equity-based loans, which use your home’s current value as collateral. Second are asset-based construction loans that look at the future value of the property. Finally, unsecured personal loans offer quick funding for smaller structural projects without risking your home’s title. Choosing the right one depends on whether you are building a simple garage or a complex structural renovation.

The Texas Section 50(a)(6) Nuance

Texas has some of the strongest consumer protections in the country regarding your home. Under Article XVI, Section 50(a)(6) of the Texas Constitution, your total home equity debt is capped at 80% of the fair market value. If your home is worth $600,000, your combined mortgage and new loan cannot exceed $480,000. When researching Home Equity Loans and HELOCs, you must also account for the mandatory 12-day cooling-off period. This state-mandated pause occurs between your application and closing. It ensures you’ve fully considered the terms before signing. Additionally, Texas law only permits one active equity loan or HELOC on your primary residence at any given time. Lender fees for these products are also capped at 2% of the loan amount, which helps keep your initial costs predictable.

Why Keller and Southlake Homeowners are Choosing Additions

Many of our neighbors in Keller and Southlake are finding that staying put and reinvesting is the strategic standard for 2026. Property values in the Dallas-Fort Worth area remain robust. Home addition costs in 2026 range between $210 and $360 per square foot in this region. When you compare this to the cost of purchasing a larger home at current market rates, building up or out is often the more fiscally responsible choice. Whether you are planning a master suite expansion or a detached ADU, working with a home addition contractor Keller TX families trust ensures your project aligns with local building codes and property value trends. The scope of your project dictates your loan choice. A smaller bump-out might be handled with a simple equity draw. A full-scale custom garage or structural renovation may require a construction loan based on the future as-completed value. This forward-looking appraisal allows you to borrow against the equity you haven’t even built yet.

Home Equity Loans vs. HELOCs: Which Fits Your Addition?

Choosing between a fixed-rate loan and a variable line of credit depends largely on the predictability of your construction schedule. Both home addition financing options Texas residents use require a clear understanding of your long-term financial goals. As of May 2026, national averages for home equity loans sit at approximately 8.05%, while HELOCs offer a slightly lower average rate of 7.28%. While these rates are higher than the historic lows of previous years, they remain a strategic way to fund expansion without disturbing your primary mortgage. Interest paid on these loans is generally tax-deductible, provided the funds are used to substantially improve the residence that secures the debt. You should always consult a tax professional to confirm how these federal rules apply to your specific North Texas property.

Lump Sum Equity Loans for Structural Stability

A home equity loan provides your total funding in a single payment at closing. This structure is ideal for projects with a defined scope and a Fixed-Price contract. Fixed interest rates provide essential peace of mind during a typical six month construction cycle. You won’t have to worry about market fluctuations affecting your monthly payment while your second story addition or garage conversion is underway. Because you receive all the cash at once, you can satisfy initial contractor deposits and material procurement costs immediately. This reliability helps maintain the momentum of your project and fosters a transparent relationship with your building team.

HELOCs for Phased Outdoor and Indoor Expansion

Home Equity Lines of Credit (HELOCs) function more like a credit card secured by your home. They are perfect for multi-phase projects, such as building an outdoor kitchen this summer and adding a master suite next year. You only pay interest on the amount you actually draw. However, Texas law imposes specific restrictions on these accounts. Every draw or advance you take must be at least $4,000. This regulation prevents homeowners from using their equity for minor, non-structural expenses. Federal agencies provide helpful consumer advice on home equity to help you understand the risks of variable rates. If the North Texas economy shifts, your interest rate and minimum payment could increase during the repayment period. Before committing to a specific lender, consider discussing your project with a local builder to ensure your financing plan matches the realistic timeline of a structural addition.

Construction Loans: Financing the “As-Completed” Value

While equity loans look back at the value you’ve already built, construction loans look forward to what your home will become. This forward-looking approach is often the most viable of the home addition financing options Texas homeowners choose when planning significant structural changes. If you are adding a detached ADU or doubling your home’s footprint, your current equity might not cover the total cost. A construction loan solves this by allowing you to borrow against the “as-completed” value of the property. Understanding How Construction Loans Work is essential because the bank essentially becomes a partner in your project. They’ll review your plans, your contractor’s history, and the projected market value of the finished home before approving the funds.

The appraisal process for these loans is more rigorous than a standard home valuation. An appraiser will analyze your architectural blueprints and the specific materials listed in your contract to estimate the property’s worth once the work is finished. This is particularly beneficial in high-value areas like Keller and Southlake, where a well-executed master suite or a custom garage can significantly boost the home’s market appeal. Instead of receiving a lump sum, the lender releases funds in stages, known as a draw schedule. This ensures the money is used specifically for the construction phases as they are completed, protecting both you and the bank from financial mismanagement mid-build.

Renovation-to-Permanent Loans

Many families prefer a renovation-to-permanent loan because it simplifies the administrative burden. You close once on a single loan that covers both your existing mortgage and the new construction costs. This “one-time close” saves you from paying double sets of closing fees and appraisal costs. To qualify, Tarrant County lenders typically require fully engineered architectural plans and a complete set of approved building permits. This structure ensures you don’t run out of cash during the critical structural phases. It provides a steady flow of capital that matches the rhythm of the build, allowing your team to focus on craftsmanship rather than funding delays.

The Vetted Contractor Requirement

Texas lenders are cautious about whom they trust with their capital. They’ll require a comprehensive builder’s package or pro-forma from your contractor before the first shovel hits the ground. Banks prioritize working with established companies that demonstrate financial integrity and a clear history of successful structural renovations. With over 25 years of professional history, we understand how to navigate these bank audits and lender inspections. We take pride in managing the complex administrative tasks required for draw requests. This includes coordinating with bank inspectors who visit the site to verify that the foundation, framing, or roofing is complete before the next tier of funding is released. This level of organization provides the peace of mind you need when managing a large-scale investment in your family’s future.

ROI and Budgeting: Making the Numbers Work in North Texas

Evaluate your home’s potential before signing any loan documents. While understanding the various home addition financing options Texas offers is vital, you must ensure the project makes financial sense for your specific neighborhood. A successful budget requires a methodical approach that balances your family’s needs with the property’s eventual market value. Start by securing a professional structural assessment. This identifies potential “hidden” costs, such as foundation issues or electrical upgrades, before they derail your financing plan. Next, compare your projected addition costs against the Tarrant Appraisal District (TAD) valuations for similar homes in your area. This data provides a realistic ceiling for your investment.

- Factor in soft costs: Remember to include permit fees, architectural design costs, and temporary living arrangements in your total loan amount.

- Prioritize high-impact spaces: Focus your budget on additions that offer the highest return on investment, such as master suites and kitchen expansions.

- Review property lines: Confirm setbacks and easements early to avoid costly design revisions later in the process.

High-Value Additions in Keller and Southlake

Market data for 2026 suggests that Master Suite additions often see a return on investment of 70% or more in North Texas. This is especially true in Keller and Southlake, where buyers prioritize luxury primary retreats. We are also seeing a massive surge in demand for multi-generational living solutions and detached ADUs. These structures provide immediate utility for families while significantly boosting the home’s appraisal value. Outdoor living remains another strong value-add. Custom patio covers and outdoor kitchens extend your home’s usable square footage at a lower cost-per-square-foot than fully conditioned indoor space.

Avoiding the “Over-Improvement” Trap

Protect your equity by ensuring your addition doesn’t exceed the neighborhood’s price ceiling. While a massive structural footprint might suit your needs, it could make the home difficult to sell later if it’s the most expensive property on the block. Work with a builder who understands local market comps in Argyle and Colleyville. They can help you build “smart” by focusing on high-quality finishes and functional layouts rather than just sheer size. This disciplined approach ensures your financing remains an asset rather than a burden. If you are ready to see how a structural expansion fits your property’s value, contact PRO Construction to schedule a professional assessment.

The PRO Construction Advantage: Design-Build and Financial Integrity

Choosing the right partner is just as important as selecting the right loan. At PRO Construction, we take a neighborly approach to managing your project’s lifecycle from the first sketch to the final inspection. We understand that structural renovations are significant investments for North Texas families. Our design-build model ensures that your architectural vision aligns perfectly with your budget. This level of coordination is essential when you’re evaluating home addition financing options Texas lenders provide. By keeping design and construction under one roof, we eliminate the communication gaps that often lead to “surprise” costs. These unexpected expenses can break a loan budget and stall your progress, so we prioritize transparency and meticulous planning to keep your project on track.

Lenders are more likely to approve funding when they see a builder with a proven reputation for stability. Our 25 years of professional history in the regional landscape eases the bank’s vetting process significantly. We provide the detailed builder’s packages and pro-forma documentation that Texas banks require for construction and renovation loans. We take pride in our highly organized administrative process; we ensure that every draw request is backed by completed work and verified inspections. This discipline protects your financial interests and builds long-term trust with both you and your financial institution.

Community Incentives and Civic Duty

We believe in giving back to those who serve our local North Texas neighborhoods. Our brand identity is rooted in gratitude, which is why we offer specialized “Service Member” incentives for community pillars. If you are a teacher, first responder, or a member of the military, we provide specific discounts to help make your dream addition more accessible. These incentives aren’t just a marketing tactic. They are a reflection of our civic duty and commitment to the people who keep our communities strong. When you are calculating your total financing plan, these savings can provide additional breathing room in your budget for high-quality finishes or structural upgrades.

Your Next Steps: From Consultation to Funding

Your journey toward a more spacious home starts with a clear understanding of your property’s structural potential. We begin with a comprehensive consultation to assess your existing foundation and roofline. This initial step sets the stage for your loan application by providing realistic cost estimates and structural feasibility reports. We help you prepare the architectural plans and permits your bank needs to finalize your funding. Don’t let financial uncertainty delay your family’s comfort. Schedule your structural consultation with PRO Construction today to build a plan rooted in integrity and consistency.

Build Your Future on a Foundation of Financial Integrity

Expanding your home in 2026 requires a balance of architectural vision and financial strategy. You now understand how the Texas Section 50(a)(6) rule limits your total debt to 80% of your property’s value; and why matching your specific project to the right loan type is essential for long-term stability. Whether you choose a fixed-rate equity loan for a garage conversion or a construction loan for a new ADU, the goal is to protect your equity while enhancing your lifestyle.

Navigating home addition financing options Texas lenders provide is easier when you have a partner who understands both the build and the bank’s requirements. With over 25 years of North Texas building experience, we specialize in managing complex structural permits and lender draw schedules so you don’t have to. We take pride in our neighborly approach and offer special incentives for teachers, first responders, and military families as a token of our gratitude for your service.

Take the first step toward your dream expansion with a team that values transparency and craftsmanship. Get a Professional Quote for Your Texas Home Addition and let’s build something that lasts for generations. Your family’s peace of mind is our highest priority.

Frequently Asked Questions

Can I finance a home addition if I have a low-interest primary mortgage?

Yes, you can secure funding without touching your original mortgage. Most North Texas homeowners choose a home equity loan or HELOC as a “second lien” to preserve their low interest rates. This strategy allows you to access the cash needed for a master suite or garage addition while keeping your primary mortgage terms exactly as they are.

What is the minimum credit score for a home improvement loan in Texas?

Lenders generally require a minimum credit score of 620 for most equity products. However, to access the most competitive home addition financing options Texas credit unions offer, you typically need a score of 740 or higher. Higher scores often result in lower interest rates and more favorable terms for structural renovations.

How long does it take to get approved for a Texas home equity loan?

The typical approval and funding process takes between 30 and 45 days. This timeline includes the mandatory 12-day “cooling-off” period required by the Texas Constitution. This state law ensures you have ample time to review the loan terms before the debt is secured against your primary residence.

Do I need a professional appraisal before applying for financing?

Yes, your lender will order a professional appraisal to determine the current fair market value of your property. If you apply for a construction loan, the appraiser will also evaluate your builder’s architectural plans. This helps them determine the “as-completed” value, which reflects what the home will be worth after the addition is finished.

Can I use a personal loan for a $100,000 home addition?

While personal loans are available, they usually feature higher interest rates and shorter repayment terms than equity-based loans. For a $100,000 project, an equity loan is often more sustainable because it offers lower monthly payments. Personal loans are generally more practical for smaller projects like a custom deck or a new pergola.

What happens if the construction costs exceed my loan amount?

Homeowners are responsible for any costs that go beyond the original loan limit. We mitigate this risk by providing detailed fixed-price contracts and conducting thorough structural assessments before work begins. It is vital to have a contingency fund in place to handle any unforeseen requirements that might arise during the structural phase.

Are there specific grants or incentives for ADUs in Tarrant County?

Direct government grants for ADUs are rare in North Texas; however, we provide specialized incentives for community pillars. We offer specific discounts for teachers, first responders, and military families to help lower the overall cost of your project. These incentives can be a significant factor when calculating your total project budget and financing needs.

How do lender draw schedules work for major structural renovations?

Lenders release funds in stages, or “draws,” as your builder reaches specific construction milestones. For example, the bank may release a portion of the funds once the foundation is poured and another after the framing is complete. A bank inspector will visit your property to verify the work before each payment is authorized to ensure financial integrity.

Disclaimer

Disclaimer: This material is for informational purposes only. While our automotive search engine optimization (SEO) strategies are designed to improve online visibility and foot traffic, we do not guarantee specific search engine rankings, website traffic volume, or vehicle sales. Search engine algorithms change frequently, and results will vary based on market competition, dealership location, website history, and other factors outside of our control. Case studies or past performance metrics shared in this material are examples of prior success and do not guarantee future results.